Identifying Vulnerable Customers

Organisations across utilities, housing and financial services are under increasing pressure from both regulators and consumers to identify vulnerable customers and provide appropriate support.

However, vulnerability is often hidden, complex and difficult to detect through traditional methods.

This guide focuses on identifying vulnerable customers, how to recognise the signs of financial hardship, and implement effective, proactive approaches to support better customer outcomes.

What is a vulnerable customer?

A vulnerable customer is someone whose circumstances make them more susceptible to harm, financial difficulty, or disadvantage when interacting with organisations or managing essential services.

Vulnerability may be caused by:

- financial hardship

- mental health challenges

- physical illness or cognitive conditions

- life events such as bereavement or job loss

Importantly, vulnerability can be temporary, permanent, or situational, and is often not immediately visible. In addition, customers are likely to experience multiple vulnerabilities at once and at multiple life stages. TellJO’s research found that the average customer qualifying for a utilities Priority Services Register has 7.1 characteristics of vulnerability. For example financial problems are often linked with increased stress and anxiety.

Research by Money and Mental Health revealed that in 2024 half of people who were behind on consumer credit bills had suicidal thoughts or feelings in the last 20 months because of the rising cost-of-living, nearly four times the rate among those not in arrears. Those with depression and problem debt are also 4.2 times more likely still to have depression 18 months later compared to those without problem debt.

A note on terminology

While ‘vulnerable customer’ is generally still the most common terminology used, after interviews with customers who have lived experience of vulnerability, there’s a move towards describing customers as ‘experiencing vulnerability’ or ‘characteristics of vulnerability’. This acknowledges both that customers move in and out of vulnerable circumstances and that being labeled as ‘vulnerable’ can feel unpleasant for customers.

Why is it important to identify vulnerable customers?

Identifying vulnerable customers early allows organisations to provide appropriate support before problems escalate.

Without effective identification:

- financial difficulty can develop into unmanageable debt

- customers may disengage or avoid contact

- enforcement actions may increase

- customer outcomes worsen

Early identification enables a shift from reactive to proactive support, improving both customer wellbeing and organisational outcomes.

As well as the risk to the customer, many sector regulators require compliance with guidelines on the fair treatment of vulnerable customers. This includes the Financial Conduct Authority’s (FCA’s) Consumer Duty, Ofgem’s Standard License Conditions and Ofwat’s Service for all guidance.

Why Vulnerability Is Often Missed

Many organisations struggle to identify vulnerability because:

- many customers do not proactively disclose sensitive information

- interactions like phone calls are often time-limited and based on providing a service quickly

- staff rely on visible or obvious indicators

- vulnerability is complex and multi-dimensional

- organisations focus on campaigns and customer segments rather than thinking of customers as individuals

Customers may avoid disclosing vulnerability due to:

- stigma or embarrassment making it difficult for someone to disclose

- avoidance and hoping the problem goes away on its own

- fear of negative consequences – reduced service, further action and enforcement

- lack of trust with an organisation, possibly due to previous bad experiences or perception based on negative media coverage

- not recognising their own situation as experiencing vulnerability or understanding that there is help available

As a result, many vulnerable customers remain undetected until debt or crisis occurs.

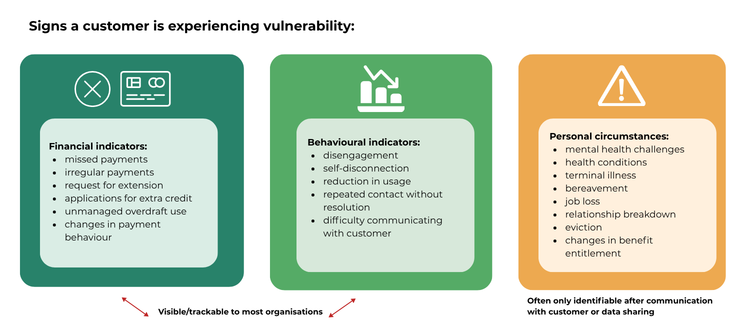

What are the signs a customer is experiencing vulnerability?

Common indicators of vulnerability include:

Financial indicators

- missed or irregular payments

- requests for payment extensions

- sudden changes in payment behaviour

Behavioural indicators

- disengagement or self-disconnection (for example vastly reduced energy usage in cold months)

- difficulty understanding information during communication

- repeated contact with a customer without resolution

Personal circumstances

- mental health challenges

- recent life event (e.g. bereavement, job loss)

- health conditions affecting daily life

Financial and behavioural indicators are ones that organisations should be able to track and identify themselves. Personal circumstances are usually only possible to spot after communication with the customer (or by data sharing with customer consent) but it’s important to note there can still be a disclosure gap with personal circumstances. For example, if a customer emails asking to change the name of an account holder due to a bereavement, with no further details or clues in the customer’s voice that would be possible to get from a phone call, it may be treated by an organisation as an administrative task – change the name and confirm to the customer with a brief line to apologise for their loss. But there is space for the organisation to look for other clues in the customer’s account to enable them to respond compassionately and proactively. They could offer signposts to bereavement support particularly for partners and family members or where to go for support with bills where the new account holder is at the same address.

It’s also worth noting that no single indicator confirms vulnerability, it is often a combination of signals.

How do organisations traditionally identify vulnerable customers?

Most organisations rely on:

- call centre conversations and staff spotting signs of vulnerability

- payment data and arrears

- customer disclosures via phone calls, emails, or online support request forms

- Data sharing agreements with local authorities, utilities, housing associations for example.

While valuable, these approaches are often:

- reactive rather than proactive

- inconsistent across teams and dependent on staff training and confidence

- dependent on customer disclosure and communication

- difficult to scale – phone calls can be time consuming, as can recording the necessary details from the conversation

They can also lead to organisations thinking they have vulnerability identification sorted as some proactive customers will self-disclose over the phone or by searching a website for help. However, these customers are the motivated few.

The FCA Financial Lives survey revealed that despite 45% of the population now being classed as vulnerable according to the FCA definition, only 27% would class themselves as vulnerable. So for organisations who have identified far lower numbers than this, vulnerability is likely being missed. But, there are ways to improve vulnerable customer identification.

A Better Approach — Proactive Identification

How can organisations identify vulnerability earlier?

A more effective approach combines:

- proactive outreach – asking if a customer is okay after a missed payment, rather than purely chasing the debt

- behavioural insights

- financial insights

- digital tools like wellbeing assessments

This allows organisations to:

- identify vulnerability before debt escalates

- understand underlying causes of vulnerability

- provide targeted support for both individual customers and specific customer groups to improve outcomes

Early identification and supportive actions and initiatives are the key to preventing long-term financial difficulty. See our blog post on increasing digital disclosure here.

The Role of Digital Wellbeing Checks

How do digital wellbeing checks help identify vulnerable customers?

Digital wellbeing checks provide a safe, structured way for customers to share information about their circumstances. Customers are five times more likely to disclose digitally and to a third party than over a phone call or in-person.

Digital wellbeing checks are effective because they tap into some of the key principles of ‘benign disinhibition’ that make up part of the ‘Online disinhibition effect’ studied by phycologist and professor John Suler in 2004.

They:

- create a private environment with a reduced fear of judgment from another person

- offer greater control as users can decide when and how much to disclose

- reduce power dynamics but introducing a third party to disclose to, rather than the service provider

- can be paused and translated or researched to allow users to gain a greater understanding of the questions, offering reduced communication pressure than a phone call

Digital wellbeing checks can also be delivered at scale. TellJO estimated they saved an energy provider an estimated £1million by replacing 30 minute phone calls to 100,000 customers with digital wellbeing checks.

For more information on the science behind why digital wellbeing checks work and why customers disclose more digitally, see the Digital Wellbeing Checks knowledge hub page.

From Identification to Action

What should organisations do after identifying vulnerability?

Identification is only the first step to supporting customers experiencing vulnerability. With knowledge on where and why customers are struggling, organisations can start to improve customer outcomes.

How to improve customer outcomes:

- tailor communication and support, this could be communications translated into a preferred language, promising to email rather than call someone who finds phone calls stressful

- offer appropriate payment solutions – matched repayments, grants and payment breaks can all be used depending on a customer’s financial situation. We’ve worked with organisations who have simply wiped debt if a customer discloses a terminal illness.

- provide referrals to support services – as talked about above debt and arrears may only be a part of the problem, repaying the debt may just be a short term solution if it is linked to things like addiction, impulsive spending and fluctuating income. Referring customers to support services that allow the customer to treat their situation holistically is more likely to create lasting improvement

- monitor outcomes for customers with a follow-up wellbeing check or analyse any patterns in usage or debt over time and adjust interventions accordingly.

How real organisations have improved outcomes:

E.ON Next used digital wellbeing checks to understand the specific mental health concerns their customers were struggling with, they then used this data to create dedicated customer care teams trained specifically in the key mental health conditions. Read a full case study on E.ON Next here.

Octopus Energy was the first UK energy company to have a dedicated social work team to support customers with complex circumstances.

DebtManagers in New Zealand use a digital wellbeing check as the first point of contact after the legally mandated confirmation letter, it allows their customers to disclose their situation without fear of judgement and allows DebtManagers to tailor the next steps to each individual customer, the process has received overwhelmingly positive feedback from customers. Read more on the partnership here.

Regulatory Expectations

What do regulators expect?

Regulators increasingly expect organisations to:

- proactively identify vulnerable customers

- understand customer circumstances

- provide tailored support

- demonstrate fair outcomes

This includes guidance from:

- The Financial Conduct Authority (FCA) Consumer Duty regulations.

- Ogem’s Standard License Conditions (SLCs) relating to vulnerability which are SLC 0, SLC 26 and SLC 27, as well as their Consumer Vulnerability Strategy.

- Ofwat’s Service for all vulnerability guidance, part of the guidance for condition G, specifically G3.5 and G3.6 of the license condition. The Service for all guidance sets out 5 key objectives and 17 minimum expectations for water companies.

- Housing sector regulation includes the Equality Act 2010, Homes (Fitness for Human Habitation) Act 2018 and the Social Housing (Regulation) Act 2023.

Organisations must comply with the relevant regulations to protect customers and tenants and minimise risks to the organisation.

Summary: Identifying vulnerable customers

Identifying vulnerable customers is essential for improving outcomes and preventing financial difficulty. Traditional methods that rely on self-disclosure alone are not enough.

By adopting proactive, structured approaches, using financial and behavioural insights and utlitising digital tools like wellbeing checks organisations can:

- identify vulnerability earlier

- understand customer needs more clearly

- reduce customer debt and arrears (up to 89% of customers sent a digital wellbeing check will request to pay)

- improve customers outcomes

- comply with regulation on the fair treatment of customers

TellJO has found customers are five times more likely to disclose digitally and to a third party than over a phone call or in-person and by asking the customer if they are okay, a wellbeing check can re-engage 33% of disengaged customers, including those in payment difficulty who may have been avoiding calls or letters.

Frequently asked questions

How do organisations identify vulnerable customers?

Organisations identify vulnerable customers through a combination of customer interactions, behavioural indicators, financial data, and structured assessments such as digital wellbeing checks.

What causes customer vulnerability?

Customer vulnerability can be caused by financial hardship, mental health challenges, life events, or health conditions that affect a person’s ability to manage services or payments.

Why is vulnerability often hidden?

Many customers do not disclose vulnerability due to stigma, lack of trust, or uncertainty about available support.

What is a disclosure gap?

A customer may disclose a part of their situation but not the full picture, meaning the vulnerability may be more entrenched or complex than first appears.